*AS curve doesn't shift in response to changes in the AD curve in the short run

- i.e.-nominal wages do not respond to PL changes

- workers may not realize impact of the changes or may be under contract (i.e. teachers don't get paid more for tutorials)

*Long run (vertical)-prd in which nominal wages are fully responsive to previous changes in PL

*when changes occur in the SR, they result in either increased/decreased producer profits-not changes in wages paid

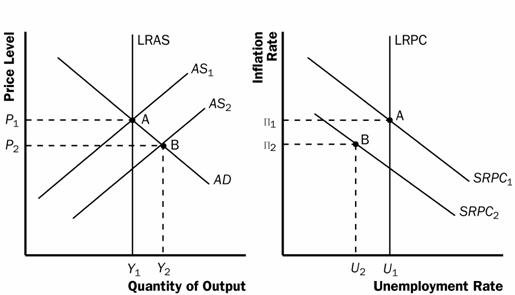

*in the LR, increases in AD result in a higher PL. As in SR, but as workers demand more $, the AS curve shifts left to equate production @ the original output level, but now @ a higher price.

*in the LR, the AS curve is vertical (LRAS) @ the natural rate of unemployment (NRU), or FE level of output. Everyone who wants a job has one and no one is enticed (lured or tempted) into or out of market.

*Demand-pull inflation will result when an increase in demand shifts the AD curve to →, temporarily increasing output while raising prices.

*Cost-push inflation results when an increase in input costs that shifts the AS curve to ←. In this case, the PL increase is not in response to ↑ in AD, but instead the cause of PL increasing. (in a recession, AD ↓ and shifts ←)